Currently, only organizations engaged in intermediary activities maintain an invoice journal: commission agents, agents, forwarders. This obligation is defined in the Tax Code of the Russian Federation. In accordance with clause 3.1 of Art. 169 of the Tax Code of the Russian Federation, VAT payers, including those exempt from taxpayer obligations, and persons who are not taxpayers, in the event that they issue and (or) receive invoices when carrying out activities on the basis of commission agreements, agency agreements providing for implementation and (or) acquisition of goods (works, services, property rights) on behalf of the commission agent (agent), are required to keep a log of received and issued invoices in relation to this activity.

In a programme 1C: Accounting 8 edition 3.0 The invoice journal is, of course, kept automatically. Any invoice received or issued creates an entry in the information register Invoice journal. And directly into the journal, register entries are selected in which the details are filled in: Invoice Amount (commission) and VAT Amount (commission). These details in invoices are filled in automatically in certain situations and are not available to the user. Everything is quite simple. But users of the program have difficulties with operations related to making corrections in the invoice journal.

The procedure for making changes to the invoice journal is defined in Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137. The journal does not use additional sheets. In accordance with clause 12 of the Journal Rules, if changes are necessary, the invoice is registered in the accounting journal for the tax period in which the invoice was registered before corrections were made to it.

The order of corrections is as follows: in a new journal line, records are made of the data on the invoice before corrections are made to it, subject to cancellation (with a negative value), and in the next line, the invoice with the corrections made to it is recorded (with a positive value).

We will look at how to do this in the program using a specific example in the accounting of an agent organization that purchases goods (works, services) for the principal on its own behalf.

Let's look at an example.

The Agent organization applies the general taxation regime - the accrual method and is a VAT payer. The organization entered into an agency agreement with the Principal organization. In accordance with the agreement, the “Agent” organization purchases services for the “Principal” organization and claims an agency fee. The Principal organization also applies the general taxation regime and is a VAT payer.

In May, a service was purchased at a cost of 118,000 rubles, including VAT 18% (18,000 rubles). The supplier issued an invoice with number 77 dated 05/30/2018 in the name of the organization (agent). The procurement report is provided to the principal on the last day of each month.

In the program, to register the transaction of acquisition by an agent for the principal of material assets and services, the document Receipt with the type of transaction is used Goods, services, commission.

The header of the document indicates the supplier counterparty and the agreement with him.

Services purchased for the principal(s) are indicated on the tab Agency services. In the tabular part, the item-service, its cost and VAT rate are selected. Each line of the tabular section indicates the counterparty-principal and the agency agreement concluded with him (type of agreement With the committent (principal) for the purchase) and settlement account.

The invoice received from the supplier is recorded in the “footer” of the document.

The Receipt document is shown in Fig. 1.

The agent must reissue the invoice received from the supplier to the principal. To perform the above operation, as well as to calculate revenue (remuneration) and VAT, the program uses the document Report to the principal with the type of operation Procurement report.

On the Main tab, the counterparty-principal and the agency purchase agreement concluded with him are indicated. The method for calculating commission (agency) remuneration, the remuneration service, the VAT rate and account, the income account and its analytics are indicated.

It is convenient to fill out the Products and Services tab automatically using the corresponding button. The tab contains two tabular parts. The top table indicates the supplier counterparties from whom the purchase was made, and the batches - Receipt documents, with the help of which the purchase operations were formalized in the program, the cost of purchased goods and services and the amount of VAT claimed by the supplier. If the supplier issued an invoice in the name of the agent, then the corresponding checkbox is turned on and the date and number of the received invoice are indicated. For each row of the upper tabular part, a lower tabular part is created. It indicates the goods and services purchased from this supplier, their cost, VAT and, if necessary, the amount of remuneration.

After filling out the document on the Main tab, an invoice for the remuneration is issued. An invoice for remuneration is registered in the sales book, but is not registered in the accounting journal (clause 3.1 of Article 169 of the Tax Code of the Russian Federation).

When carrying out the document in accounting and for profit tax purposes, it will accrue revenue (remuneration), charge VAT on the revenue and, to register an invoice for remuneration, make an entry in the Sales VAT accumulation register.

The document Report to the committent is shown in Fig. 2.

And what is most important for us now is that when conducting (recording), the document will re-issue invoices received from suppliers in the name of the principal (will create documents Invoice issued) and write down links to these invoices in the upper table part in the Invoice attribute.

The agent issues an invoice with the date of the invoice received from the supplier. In our example, the principal was issued an invoice numbered 13 dated May 30, 2018. In the issued invoice, as expected, the supplier is indicated as the seller, and the principal is indicated as the buyer.

The printed form of the issued invoice is shown in Fig. 3.

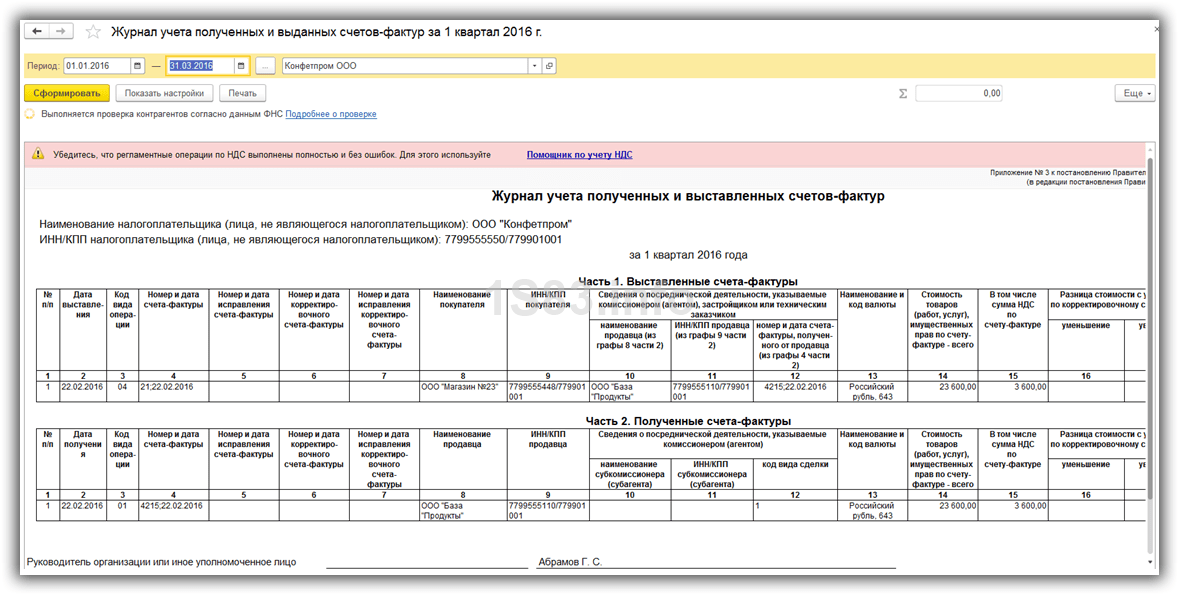

Let's look at the invoice log. Part 2 “Received invoices” records invoice No. 77 dated 05/30/2018 received from the supplier in the amount of 118,000 rubles, including VAT of 18,000 rubles. In Part 1 “Issued invoices”, invoice No. 13 dated May 30, 2018, issued in the name of the principal, is registered. In column 8 the buyer-principal is indicated, in column 10 the supplier is indicated and in column 12 the invoice issued refers to the invoice received from the supplier. The log is filled out correctly.

The invoice journal is shown in Fig. 4.

Now let's look at what corrections might theoretically be needed in our wonderful invoice journal. Let's consider three cases.

First case. The supplier found errors in the source documents. The cost of the service provided was incorrectly indicated (inflated). The real (correct) price is 106,200 rubles, including VAT 18% (16,200 rubles). The supplier issued a corrected invoice to the agent, correction No. 1 dated July 30, 2018 to invoice No. 77. The agent needs to reissue the corrected invoice received from the supplier to the principal.

First, let's document in the program the fact of receiving a corrected invoice from the supplier. Let’s open (or not open) the document Invoice received No. 77 dated 05/30/2018 and use the “Create based on” button. In the menu that opens, select the item Invoice correction(Fig. 5).

The program has two special adjustment documents: Adjustment of receipts And Implementation adjustments. These documents are used to register corrected and adjusted invoices received from suppliers and issued. Therefore, it is not surprising that the program opened the Receipt Adjustment document for us (it can also be created based on the Receipt document).

On the Main tab, the type of operation and the basis document have already been selected - the Receipt document, with the help of which the purchase of goods (works, services) for the principal was registered. The adjustment will be reflected in all sections of accounting.

Tabular part on the tab Agency services When you select the base document, it is filled in automatically. The table part line contains two substrings: “before the change” and “after the change”. In the “after change” substring, you must manually change the price in accordance with the document received from the supplier.

The corrected invoice received from the supplier is registered in the “footer” of the document.

The Receipt Adjustment document is shown in Fig. 6.

Open the registered (created) document Invoice received for receipt 77 (correction 1). The document refers to invoice No. 77 dated May 30, 2018. The basis document is the document Adjustment of receipts(Fig. 7).

To reissue a corrected invoice to the principal, the agent needs to find the document Invoice issued No. 13 dated 05/30/2018 and, as in the previous operation, use the “Create based on” button. In the menu that opens, also select the item Invoice correction(Fig. 8).

In this case, we will create a document Implementation adjustments with the type of operation Correction in primary documents. The basis is the document Invoice issued, reflection of the adjustment is possible only in VAT accounting (but nothing else is required).

The tabular part, in this case on the Services tab, is filled in manually. The “before change” substring indicates the price before the error was corrected, and the “after change” substring indicates the correct price.

The corrected invoice issued to the principal is issued in the “basement” of the document.

The Implementation Adjustment document is presented in Fig. 9.

When carried out, the document does not make any movements, it only serves as the basis for document C invoice issued for sale 13 (correction 1).

The above document and its printed form are presented in Fig. 10.

Everything seems to be fine, but let’s look at the result of the document.

The document, as prescribed in the Rules for maintaining an invoice journal, reversed (with a minus sign) the erroneous entry and added (with a plus sign) a new correct entry to the information register Invoice journal. But for some reason I didn’t fill in the details in the new entry. Supplier invoice number, which means that column 12 of part 1 of the journal will not be filled in.

To correct this shortcoming, I can only suggest turning on the “Manual adjustment” checkbox and entering the invoice number manually (Fig. 11).

Let's see what we got in the invoice journal. In part 2 of the journal, the erroneous entry was canceled and a correction was registered in the received invoice No. 1 dated July 30, 2018 in the amount of 106,200 rubles, including VAT of 16,200 rubles. In Part 1, the erroneous entry was also canceled and the correction to the issued invoice was registered. In column 12, the invoice issued refers to the invoice received from the supplier. Everything turned out right.

The invoice log after correcting the error is shown in Fig. 12.

Second case. When registering an invoice received from a supplier, the agent made a technical error when entering the cost of the service and, in addition, entered the invoice number incorrectly (for example, instead of number 777, number 77 was entered). The agent needs to make adjustments to the invoice journal: correct his own error and issue a corrected invoice to the principal.

To correct an error made when registering a supplier invoice, we will find a document Invoice received No. 77 dated 05/30/2018 and again use the “Create based on” button. In the menu that opens, now select the item (Fig. 13).

As in the previous case, a document will be created Adjustment of receipts, but with the type of operation Correcting your own mistake.

When using this type of operation, a special block appears on the Main tab for correcting errors in the invoice details, which consists of two columns of details: “Old value” and “New value”. We will indicate the new, correct value of the received invoice number.

We will correct the error in the cost in the tabular section on the tab. Agency services exactly the same as in the previous example.

Using the “Register” button, we will register the corrections we have made in a special document.

Document Adjustment of receipts shown in Fig. 14.

As a result of our actions, a special official document will be created Invoice received, designed to correct “our own” errors when registering invoices from the supplier (Fig. 15).

We will not consider the process of issuing a corrected invoice to the principal a second time (it is discussed in detail in the first example), but will immediately attend to our invoice journal.

Part 2 of the journal cleared the erroneous entry and recorded the correct entry with the corrected invoice number and correct amounts. In Part 1 of the journal, the erroneous entry was canceled and a corrected invoice was issued that referenced invoice No. 777.

The invoice journal is shown in Fig. 16.

Finally, let's consider the third case. The agent mistakenly recorded an invoice from the supplier in the accounting journal and also mistakenly (automatically) reissued it in the name of the principal. Invoice entries in the accounting journal must be cancelled.

The rule is very simple. In accordance with clause 12 of the Journal Rules, in the event of an erroneous registration of an invoice in the journal, records of the invoice data are made in a new line of the journal, subject to cancellation (with a negative value) for the tax period in which the specified invoice was erroneously registered -texture.

As we know, a journal entry is an information register entry Invoice journal. An entry in any information register cannot be automatically reversed, and there is no special document in the program for this purpose. Therefore, we will have to make entries in the register Invoice journal manually. The adjustment can be made using the document Operation, but this is quite labor-intensive, since the register contains a lot of details. Therefore, I propose to make adjustments to document movements Invoice received No. 77 dated 05/30/2018 and Invoice issued No. 13 dated May 30, 2018, since the result of carrying out these documents is the invoice journal entries we need.

Let's start with the invoice we received. To make adjustments, you need to enable the checkbox in the document posting results Manual adjustment. After this, you need to copy the register entry and set the minus sign in the amounts in the new entry. Additionally, you must enable the Reversal checkbox and the Reversal checkbox in the copied register entry. Correcting your own mistake.

The result of adjusting document movements Invoice received presented in Fig. 17.

Document movements Invoice issued are adjusted in exactly the same way.

Let's look at the invoice log for the last time. As we can see, in both parts of the log, erroneous entries were successfully canceled.

The invoice journal is shown in Fig. 18.

Everything turned out to be quite simple. Probably, this production option - without using planned cost - will be convenient for someone.

Liked? Share with your friends

Consultations on working with the 1C program

The service is open specifically for clients working with the 1C program of various configurations or who are under information and technical support (ITS). Ask your question and we will be happy to answer it! A prerequisite for obtaining consultation is the presence of a valid ITS Prof. agreement. The exception is the Basic versions of PP 1C (version 8). For them, a contract is not necessary.

This document is issued by the seller after the buyer actually receives any goods or services from him. In the Russian Federation, an invoice is required only for, it is issued by those sellers who are obliged to pay it.

Based on received invoices, the VAT taxpayer creates a “Purchase Book”, and based on issued invoices, a “Sales Book”.

In 1C 8.3 Accounting 3.0, there are received and issued invoices. They are adjustable, for an advance and for an advance of the principal. Invoices issued are also for sales and the tax agent. Those received, in turn, in addition to those listed above, may be eligible for admission.

All these documents are most often created from sales and receipt documents. In this article we will look at how to create all possible invoices in 1C 8.3 Accounting.

Creating a document for implementation

As an example, let's open any implementation document from the demo database. At the very bottom of the form you will see the “Write an invoice” button.

After clicking on this button, the program will automatically create a fully completed “Invoice” document. You can open it using the hyperlink that appears in place of this button.

You can print an invoice directly from the sales document by clicking the “Print” button.

In the resulting invoice, you can indicate the delivery method: on paper or electronically. The second method is usually applicable in cases where your organization and counterparty are connected to an electronic document management system. In such a situation, sending and receiving documents can be carried out directly in 1C.

How to create a new sales document and an invoice for it, watch the video:

For advance

Before you begin, you need to make some preliminary settings.

Go to setting up taxes and reports. In the “VAT” section we will need to change the “Procedure for registering advance invoices”.

For our example, we will select from the drop-down list the item “Do not register invoices for advances offset until the end of the tax period.”

In such a situation, invoices will be issued only at the end of the reporting period. Setting this setting will allow us to significantly reduce the number of documents because only those advances will be taken into account for which there was no shipment of goods or the fact of provision of services at the end of the quarter.

In addition to setting this setting for the organization as a whole, you can also specify it for a specific agreement with a counterparty. To do this, open the card of the corresponding agreement and go to the “VAT” section. This is where a similar setting is located.

The process of issuing invoices for advance payments is carried out using the VAT accounting assistant. It is located in the Operations menu.

This processing includes a routine operation for registering advance invoices. The line below allows you to register tax agent invoices. This functionality is only available under contracts with the appropriate feature.

Video on generating advance invoices:

Invoices received

For admission

Let's consider the reflection of received invoices from the document “Receipts (acts, invoices)”. Here everything is even simpler than in creating issued invoices for sales.

At the bottom of the form you just need to enter the number and date of the document received. After that, click “Register”.

After clicking on this button, the program will automatically create a fully completed invoice and insert a link to it into the receipt document.

For advance

This type of invoice can be created upon receipt of DS, both to the company’s bank account and to the cash register. In this case, we create based on cash receipts.

Invoices for the advance payment of the principal are created for those contracts that have this attribute.

Adjustment invoices

These types of invoices can be either for receipt or for sale. They are taken into account accordingly.

We will not consider an example of creating both types of invoices, since the actions in both cases are almost identical.

Let’s open any implementation document from the demo database and create an “Implementation Adjustment” document based on it.

Let's say we agreed with the buyer that he will buy more anniversary cookies and classic mini-croissants. For this we will give him a discount on Tyrolean blueberry pie.

In the newly created implementation adjustment document, each line item has two lines: with the values before the change and after. After we have made all the necessary changes, click on the “Write an adjustment invoice” button, which is located in the usual place at the bottom of the form.

The invoice will be created and filled out automatically and will be available via the appropriate hyperlink.

Video on creating an adjustment invoice from a seller:

Verification of documents

To analyze and find documents for which there are no invoices, you can use a special processing in the program called “Express check”. It is located under the “Reports” menu.

The figure below shows an example of displaying errors for a problem of interest to us, as well as recommendations proposed by the program.

Invoice journal

Movements of the document “Invoice”

If you open the postings of any invoice, you can see that no entries are created in the accounting registers. The document is reflected in the information register “Invoice Log”.

Journal of received and issued invoices

This report is located in the Reports menu.

In the header, indicate the period (usually a quarter) and organization. If the program detects any errors, a corresponding message will be displayed.

Decree of the Government of the Russian Federation of August 19, 2017 No. 981

A comment

On October 1, 2017, amendments made to the Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 “On the forms and rules for filling out (maintaining) documents used in calculations of value added tax” came into force.

The amendments affected the forms and rules for filling out (maintaining) invoices, purchase books and sales books, as well as a journal for recording received and issued invoices. Let's take a closer look at the most significant ones.

Invoices

From July 1, 2017, the invoice form has already been updated by Decree of the Government of the Russian Federation dated May 25, 2017 No. 625, when, in accordance with paragraphs. 6.2 clause 5 and clauses. 4.2 clause 5.1 art. 169 of the Tax Code of the Russian Federation, a new line 8 “Identifier of the state contract, agreement (agreement)” appeared. From October 1, 2017, this new line slightly changed the name to “Identifier of the government contract, agreement (agreement) (if any).” Let us recall that this line indicates the identifier of the state contract for the supply of goods (performance of work, provision of services), contract (agreement) on the provision of subsidies from the federal budget to a legal entity, budget investments, contributions to the authorized capital. The basis for filling out this line is the execution of contracts in accordance with Federal Law dated December 29, 2012 No. 275-FZ and Decree of the Government of the Russian Federation dated December 30, 2016 No. 1552. Since there is no indication of the need to put a dash in the rules, failure to fill out line 8 is not a violation and meets the requirements of the law (letter of the Ministry of Finance of Russia dated September 8, 2017 No. 03-07-09/57870).

In addition, a new column 1a “Product Type Code” has appeared in the invoice form, which meets the requirements of paragraphs. 15 clause 5 art. 169 of the Tax Code of the Russian Federation and is completed in relation to goods exported outside the territory of the Russian Federation to the territory of a member state of the EAEU. In the absence of this indicator, the rules require putting a dash in the column.

Column 11 of the invoice is now called “Registration number of the customs declaration”. Therefore, it must indicate the 23-bit number from column “A” of the main and additional sheets of the goods declaration, formed in accordance with paragraphs. 1 clause 43 of the Instructions on the procedure for filling out the declaration of goods, approved. by decision of the CU commission dated May 20, 2010 No. 257.

In the invoice signatories, an indication appeared that the invoice can be signed not only by an individual entrepreneur, but also by another person authorized by him, which corresponds to the provisions of clause 6 of Art. 169 Tax Code of the Russian Federation.

Significant clarifications have been made to the rules for filling out invoices.

Now the rules set out the procedure for filling out invoices issued by forwarders, developers (customers performing the functions of a developer) to buyers (clients, investors), although the term “consolidated invoice” itself still did not appear in Resolution No. 1137.

Unlike an invoice drawn up by a commission agent (agent) purchasing goods (work, services), property rights from two or more sellers on his own behalf, such a “consolidated invoice” can be generated by forwarders and developers on the basis of invoices compiled by sellers for different dates. In this case, the “consolidated invoice” indicates the date of preparation of such an invoice by the forwarder or developer himself, and the name and tax identification number (TIN) of the forwarder or developer himself is given as the seller. The rules also stipulate that the “consolidated invoices” of forwarders list the names of the goods supplied (description of work performed, services provided), transferred property rights in separate positions for each seller, and in the “consolidated invoices” of developers - the names of the construction and installation work performed, purchased goods (works, services), property rights in the context of individual items only.

The clarifications also affected the procedure for indicating the address on the invoice. Now the rules require reflecting the address (for legal entities) specified in the Unified State Register of Legal Entities within the location of the legal entity and the place of residence (for individual entrepreneurs) specified in the Unified State Register of Legal Entities. Let us recall that previously the rules required indicating the location in accordance with the constituent documents or the place of residence of the individual entrepreneur. Such changes are not aimed at tightening the requirements for the structure and accuracy of the address. They are connected mainly with the fact that, in accordance with paragraph 2 of Art. 54 of the Civil Code of the Russian Federation, the location of a legal entity is determined by the place of its state registration on the territory of the Russian Federation by indicating only the name of the locality (municipal entity). At the same time, according to paragraphs. 2 p. 5, pp. 2 clause 5.1, paragraphs. 3 clause 5.2 art. 169 of the Tax Code of the Russian Federation, invoices must indicate the specific address of the taxpayer.

The filling rules specify the procedure for storing invoices in chronological order by the date of their issuance (composition) or receipt for the corresponding tax period.

Adjustment invoices

Changes were made to the adjustment invoice form, similar to changes in the invoice form:

- line 5 became known as “Identifier of the state contract, agreement (agreement) (if any)”;

- column 1b “Product type code” appeared;

- the list of signatories mentions another person authorized to sign invoices on behalf of the individual entrepreneur.

In the rules for filling out an adjustment invoice, only one new provision has appeared, according to which the taxpayer has the right to indicate additional information in additional lines and columns of the adjustment invoice, including details of the primary document (provided that the form of the adjustment invoice is preserved). Thus, technically, a rule has been added that was previously introduced for invoices and has already been actually implemented in the universal adjustment document.

Invoice journal

The form of the accounting journal has changed slightly. Thus, technical amendments were made to the general title of columns 10-12 (now – “Information from invoices received from sellers”) and to the title of column 12 (now – “number and date of the invoice (adjustment invoice), received from the seller (from column 4 (column 6) of part 2)").

The list of signatories mentions another person authorized to sign the invoice journal on behalf of the individual entrepreneur.

Serious clarifications have been made to the rules for maintaining the accounting journal.

First of all, in accordance with clause 3.1 of Art. 169 of the Tax Code of the Russian Federation, the rules confirm the obligation to maintain an accounting log only by intermediaries, forwarders and developers. It is also indicated that the journal is not kept when commission agents (agents) sell goods (work, services) to the persons specified in paragraphs. 1 clause 3 art. 169 of the Tax Code of the Russian Federation, and in cases provided for in paragraph 5 of Art. 161 Tax Code of the Russian Federation.

Both in part 1 and in part 2 of the accounting journal form, columns 2 “Date of issue” and “Date of receipt” are still retained, respectively, but these dates are no longer of fundamental importance for determining the tax period for registering invoices. According to the rules for maintaining an accounting journal, now in Part 1, invoices compiled for the expired tax period are registered, and in Part 2 - invoices compiled for the expired period and received, incl. after the end of the tax period in which the invoice was drawn up for the buyer, but before the deadline for submitting the declaration or the deadline for submitting the journal under clause 5.2 of Art. 174 Tax Code of the Russian Federation. By the way, the provisions describing the procedure for indicating information in columns 2 of part 1 and part 2 of the accounting log are excluded from the rules for maintaining the accounting log, which means, according to representatives of the Federal Tax Service of Russia, that these columns should no longer be filled out at all.

The previously recommended procedure for making corrections to the accounting journal, previously recommended by the Federal Tax Service of Russia, has been fixed. Thus, the corrected invoice is recorded in the accounting journal for the period in which the invoice was registered before the corrections were made to it. In this case, the entry on the invoice is canceled before corrections are made to it and the corrected invoice is registered. In the event of an erroneous registration of an invoice, the entry for the tax period in which such an invoice was registered is canceled. If it is discovered that an invoice has not been registered in the accounting journal, the data on such an invoice is recorded for the tax period in which the invoice was drawn up.

The procedure for registering invoices in the event of the sale or acquisition of goods (work, services), property rights by commission agents (agents) in various situations is described in detail.

So, for example, if a commission agent (agent) sells both his own goods (work, services) and the goods (work, services) of the principal (principal), then in part 1 of the accounting journal he reflects in column 14 the total cost from column 9 on the line " Total payable" invoice, and in column 15 - the amount of VAT in relation to goods (work, services) sold under a commission agreement (agency agreement). If the commission agent (agent) sells goods (work, services) of several principals (principals), then the registration procedure will be slightly different. In this case, in part 1 of the accounting journal, column 14 will reflect the cost of goods (work, services) from column 9 in the line “Total payable” for each invoice issued by the principal (principal) to the commission agent (agent). Accordingly, in column 15 the amount of VAT from column 8 will be indicated in the line “Total payable” for each invoice issued by the principal (principal) to the commission agent (agent). Obviously, the various registration rules do not give a clear answer to the question of what should be done if both the commission agent’s (agent’s) own goods (work, services) and the goods (work, services) of several principals (principals) are simultaneously sold. In accordance with the comments of representatives of the Federal Tax Service of Russia, in this case one should be guided by the procedure that is provided for the sale of goods (works, services) of several principals (principals).

The maintenance rules indicate the possibility of registering customs declarations and applications for the import of goods and payment of indirect taxes in Part 2 of the journal (with the transfer of this data to columns 10-12 of Part 1 of the accounting journal). However, the procedure for re-issuing invoices based on data from customs declarations and import applications is provided only for forwarders and developers, i.e. only for cases of generating “consolidated invoices”, which reflect (including) information on the amounts of VAT paid when importing goods into the territory of the Russian Federation.

A special procedure for filling out the accounting log is established for intermediaries purchasing goods (works, services) from foreign entities for Russian principals (principals) and acting tax agents. It provides for the obligation to register in part 2 of the logbook of one’s own invoices issued in the performance of the duties of a tax agent, and in part 1 - also one’s own invoices, but already re-issued to the principal (principal) on the basis of data from invoices issued as a tax agent. agent.

As was determined in the previous edition of Resolution No. 1137, the journal of invoices must be compiled before the 20th day of the month following the expired tax period. This is due to the fact that persons who keep an accounting log, but do not submit a VAT tax return, are required to send to the tax authorities a log of received and issued invoices in the established format in electronic form via TKS through the EDI operator no later than The 20th day of the month following the expired tax period (clause 5.2 of Article 174 of the Tax Code of the Russian Federation).

Sales book (additional sheet of sales book)

New columns have appeared in the form of the sales book (an additional sheet of the sales book):

- column 3a "Registration number of the customs declaration";

- column 3b "Product type code".

Both columns are filled in only in exceptional cases. Thus, column 3a indicates the registration number of the customs declaration issued upon release of goods in accordance with the customs procedure for release for domestic consumption upon completion of the customs procedure of the free customs zone on the territory of the Special Economic Zone in the Kaliningrad Region (in accordance with paragraph 1.1, paragraph 1 Article 151 of the Tax Code of the Russian Federation).

And in column 3b the code of the type of goods is given in accordance with the Commodity Code of Foreign Economic Activity of the EAEU only in relation to goods exported outside the territory of the Russian Federation to the territory of a member state of the EAEU.

A small technical clarification has been made to the general title of columns 17 and 18 of the sales book.

There was also an indication of the possibility of signing the sales book by an authorized person of the individual entrepreneur.

The rules of conduct now contain a provision according to which, in the event of failure to issue invoices in accordance with paragraphs. 1 clause 3 art. 169 of the Tax Code of the Russian Federation, primary accounting documents and documents containing summary (consolidated) data on transactions performed during a calendar month (quarter) are registered in the sales book. When prepayment amounts are received as part of such transactions, payment and settlement documents or documents containing summary (summary) data on the prepayment amounts received during the calendar month (quarter) are registered in the sales book. The procedure for registering documents for an increase in value in the absence of adjustment invoices is similarly prescribed.

The procedure for registering invoices issued by intermediaries when selling their own goods (work, services) and goods (work, services) of principals (principals) has been clarified. In this case, column 13b indicates the cost of all goods (work, services) from column 9 on the “Total payable” line of the invoice, and in columns 17 and (or) 18 - the amount of VAT only in relation to your own goods (work, services) ).

When transferring property, intangible assets, property rights as a contribution to the authorized (share) capital of business companies and partnerships or share contributions to mutual funds of cooperatives to reflect the restoration of VAT amounts in accordance with paragraphs. 1 clause 3 art. 170 of the Tax Code of the Russian Federation, the sales book must now record those documents used to formalize such a transfer.

Like the VAT return, the sales ledger must be prepared by the 25th day of the month following the expired tax period.

Purchase book (additional purchase book sheet)

In the form of the purchase book (an additional sheet of the purchase book), clarifications were made to the names of individual columns:

- in the general title, columns 11 and 12 now mention not only intermediaries (commission agents, agents), but also forwarders and persons performing the functions of a developer;

- Column 13 became known as “Registration number of the customs declaration”.

The form also contains an indication of the possibility of signing the purchase book by an authorized person of the individual entrepreneur.

The main change in the rules for maintaining a purchase ledger was the removal of the requirement to register corrected invoices as the right to a tax deduction arose, which was interpreted by the tax authorities as a requirement to register corrected invoices in the tax period of their actual receipt. To confirm the legality of registering the corrected invoice in the same tax period in which the invoice was registered before the corrections were made to it, the following procedure was prescribed in the rules for filling out an additional sheet of the purchase book. When summing up the results in column 16 in the “Total” line, the indicators of the invoice records subject to cancellation are subtracted from the indicators in the “Total” line and the indicators of registered invoices with corrections made to them are added to the result obtained.

Also excluded is the indication of the illegality of registering advance invoices in the purchase book for non-cash forms of payment, which corresponds to the legal position of the Supreme Arbitration Court of the Russian Federation (clause 23 of the resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated May 30, 2014 No. 33).

It has been established that in order to claim a tax deduction for VAT amounts calculated from the prepayment received, payment and settlement documents or other documents containing summary (summary) data are registered in the purchase book in the absence of invoices, i.e. the same documents that were previously recorded in the sales book for tax purposes.

The procedure for determining the cost of goods imported into the territory of the Russian Federation has been clarified for filling out column 15:

- when importing goods from the territory of states that are not members of the EAEU, the cost of goods reflected in the accounting shall be indicated;

- When importing goods from the territory of the EAEU member states, the tax base from column 15 of the application for the import of goods and payment of indirect taxes is reflected.

The rule is established according to which, in the case of an intermediary purchasing goods (work, services) both for himself and for the principal (principal), in column 15 the cost of all goods (work, services) from column 9 is indicated in the “Total payable” line of the invoice , and in column 16 - the amount of VAT only in relation to own acquisitions.

The specifics of registering a single adjustment invoice are prescribed, according to which in column 3 of the purchase book the number and date of the single adjustment invoice is repeated, and column 4 is not filled in at all. It is also necessary to note that in the event of a decrease in the cost of shipped goods (work, services), property rights, when the seller registers a single adjustment invoice in the purchase book, columns 9 and 10 indicate information not about the seller, but about the buyer from lines 3 “Buyer " and 3b "TIN/KPP of the buyer" of a single adjustment invoice.

The procedure for registering in the purchase book of invoices received during the acquisition of goods (work, services), property rights for carrying out transactions taxed at a tax rate of 0 percent (in accordance with paragraph 1 of Article 164 of the Tax Code of the Russian Federation) has been brought into compliance with the Tax Code of the Russian Federation. . We would like to remind you that from July 1, 2016, the requirement to declare a tax deduction for purchased goods (work, services) at the time of determining the tax base does not apply to the export of non-raw materials, as well as to the sale of precious metals by taxpayers engaged in their extraction or production from scrap and waste containing precious metals, the State Fund of Precious Metals and Precious Stones of the Russian Federation, funds of precious metals and precious stones of the constituent entities of the Russian Federation, the Central Bank of the Russian Federation, banks.

Like the VAT return, the purchase ledger must be prepared by the 25th day of the month following the expired tax period.

Why is invoice accounting necessary? How to maintain it? What documents need to be used for this? Why is a log of invoices received and provided generally necessary? We will answer these and many other questions in today’s article.

What is an invoice: issued, received?

An invoice is a document drawn up according to a strictly established template as a result of the sale of inventory items. Such a document serves as the basis for deduction from value added tax. It can be either received from a counterparty - such a document allows the organization to deduct the amount of VAT, or issued - which allows the counterparty of the organization providing it to take advantage of the deduction.

Why do you need to take into account issued and received invoices?

Received and issued invoices allow both the organization itself and its counterparty to reduce the tax base for calculating VAT. However, in order to have the right to use such a deduction, it is necessary to take into account the documents issued and received that are its basis. At any time, the tax authority may have doubts about the legality of such a deduction and may demand the provision of supporting documents. The tax office may also request information on invoices in cases where they are checking any counterparty of this organization.

Important! If invoices are not taken into account and stored, then as a result of an inspection by the Federal Tax Service of Russia, the inspector may consider the tax deduction to be unlawful. As a result, the VAT will be recalculated again, and the organization will be obliged to pay not only the difference in already paid and accrued VAT, but also the fine imposed for a gross violation, as well as the amount of penalties calculated for the entire period of non-payment.

Speaking of document storage: the storage period for invoices cannot be less than five years.

Whose responsibilities include maintaining invoice records?

Keeping records of invoices, both issued and received, is part of the responsibilities of accounting employees. As a rule, the organization of accounting is entrusted to the chief accountant, who distributes responsibilities among subordinates. Often, keeping records of invoices is entrusted to the accountant responsible for the acquisition and sale of inventory, much less often this is done by accountants of other profiles, or even more so by the chief accountant himself.

What document should I use to record invoices?

Keeping records of these documents involves maintaining a specialized journal of invoices. It is a tax register and is required to be submitted quarterly to the tax authorities of the Russian Federation. Based on it, the tax office reconciles your reporting with your actual accounting.

Important! However, not all organizations are required to honor invoices. Companies using the simplified tax system may not issue these documents to each other. In this case, an appropriate agreement is concluded, which stipulates the conditions for non-provision of invoices.

What is the procedure for registering issued and received invoices?

As mentioned earlier, the log of invoices received and issued must be completed quarterly. It consists of two large sections. The first section is issued invoices. It contains information about issued documents indicating the transaction code, document number, date, etc. In the second section – Received invoices – information about invoices is entered in the order in which they were received.

This document can be maintained in paper or electronic form, but the tax office requires the provision of only its electronic version.

Where can I download a form and sample invoice book?

The invoice journal form is available for download on almost any information resource dedicated to accounting. You can also download it.

Every company must keep a log of invoices that have been received and issued for a given tax period. It can be electronic or classic paper with stitching and page numbering, as well as a company seal.

The basis of this document is made up of two tables: one of them takes into account issued invoices, and the second - received invoices, and all of them are subject to mandatory registration in strict adherence to chronological order.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

The rules require the enterprise to keep the journal for a four-year period, along with all primary documents that serve as confirmation of VAT deduction.

Basic provisions

Who is required to register

The question of who submits the logbook was regulated by changes in legislation that came into force at the beginning of 2019.

If previously filling out was the responsibility of each enterprise, regardless of its type of activity, provided that it works with invoices, now this should only be done by:

- intermediaries acting on their own behalf, but in the interests of the customer with whom the relevant agreement has been concluded;

- conducting activities related to transportation services;

- those who act as developers on their own plot of land.

Registration must be carried out by both individual entrepreneurs and legal entities. persons, regardless of what taxation system they use.

Cancellations and changes to the rules

In April 2019, changes were made to the legislation regulating tax and accounting aimed at making the accounting process simpler.

The main innovations are as follows:

- keeping invoice logs is optional for VAT taxpayers;

- the invoice form can be signed not by the entrepreneurs themselves, but by persons who have the appropriate authority to do so;

- VAT on the sale of real estate is calculated at the moment when the property is directly transferred to the new owner;

- changes have been made to the rules regarding amount and exchange rate differences, which are combined under the general term “exchange differences”;

- the obligation to record expenses for equipment and workwear at a time has been cancelled;

- a procedure has been established by which property received or transferred free of charge is taken into account in value (its market value can be written off as expenses);

- excluded from tax accounting;

- the issue of including the loss from the assignment of the right to claim a debt in the category of expenses has been clarified (in 2019, the negative difference between the income received from the sale of the right to claim a debt and the price of the product/service is taken into account in expenses on the date when the purchase was made).

Books of purchases and sales

From August 2019, new forms of both the accounting journal and the books of acquisitions and sales are subject to application.

The following changes have occurred in the purchase book:

| 2nd column | It appeared under the name “Operation Type Code”. |

| 3rd column | Regarding the number and date of the seller's invoice, now the customs declaration number or the number with the date of the statement regarding the import of goods and payment of indirect taxes is entered, depending on the country from which the goods are imported. |

| 7th Earl | Involves entering details of documents that serve as confirmation of the actual payment of VAT. |

| 11th and 12th columns | Concerns information and activities of intermediaries. |

| 14th Earl | Intended for the name and code of the currency, the filling of which is required only in cases where the purchase of goods occurs in foreign currency. In all other situations, it is not filled, that is, it remains empty. |

The sales book was not without changes. In particular, there is no longer a need to include adjustment invoices, which are drawn up by the seller, if there is an increase in the cost of shipped products within the tax period when the shipment itself took place.

In addition, the following columns were added to the form:

Requirements for filling out the invoice journal

The basic requirements that should be followed when filling out an invoice journal are quite few. One of the main requirements concerns the mandatory presence of document page numbering. In addition, it must certainly be stitched.

If you use computer programs, for example 1C 8.3, to maintain a log, the registers must necessarily be output to paper with numbering and firmware.

The company that maintains the accounting journal independently has the right to determine over what time period it will be formed. Ignorance of this document does not provide for any other liability other than a 50-ruble fine in accordance with Article 126 of the Tax Code of the Russian Federation.

Legal transactions

The consignor's goods and yours

If the intermediary acts at the same time as both a commission agent (agent) and a supplier, then the buyer is invoiced for the full volume of goods. In this case, the intermediary indicates himself directly as the seller, despite the fact that the principal’s goods are also present there.

The invoice goes through the registration process in the sales ledger, as well as the intermediary ledger and the customer's purchase ledger. After this, the invoice data is sent to the principal so that he can reissue the document to the intermediary.

This reissued invoice reflects exclusively the goods the owner of which is the principal. Registration is required in the principal's sales ledger and in the intermediary's ledger.

For the principal (principal)

When purchasing goods by an intermediary personally on his own behalf for the principal, the supplier issues an invoice in the name of the intermediary. The registration must be made in the intermediary's register, in its acquisition book and in the supplier's sales book.

Summary Variations

It is allowed for the intermediary to issue a consolidated invoice in the name of the principal, including goods purchased from various suppliers. Likewise, the principal may issue a consolidated invoice to include items sold to multiple customers.

In the case of the sale of goods belonging to the principal to a plurality of customers, separate invoices are issued in the name of each of them, which are entered in the corresponding purchase books.

After this, the principal receives data from the intermediary regarding all sales made, and the principal, in turn, issues a general invoice for the volume of goods sold. This general account is recorded in the intermediary's journal and the principal's sales ledger.

When an intermediary purchases goods for the consignor, he is presented with invoices from the suppliers. These issued documents are subject to registration in the register and sales books of the suppliers. After this, the consignor is issued a general invoice from the intermediary for the goods purchased from all sellers. The recording of this aggregate account is carried out in the intermediary's journal and the principal's acquisitions ledger.

There are cases when an intermediary receives an advance payment from a number of buyers on one day for the future delivery of goods that belong to the principal. In this case, the responsibility of the intermediary is to issue separate invoices for advances to each of the clients. These invoices must be recorded in the journal and purchase books of these customers.

Subsequently, the principal receives a message from the intermediary regarding all advances, and the principal issues a general invoice for advances, recorded in the intermediary's journal and the principal's sales book.

Other situations and solutions

Nuances for commission agents

If commission agents purchase any goods on their own behalf for the principals, then the conclusion of an agreement occurs between the commission agents and the sellers. When providing an invoice for the purchase of products on your own behalf based on invoices from sellers, a sample commission agent form must be kept in the journal.

Important points that must be taken into account by the commission agent:

- for the remuneration received by him, forms must be provided to the principals (both for the remuneration itself and for the goods);

- invoices accepted from sellers are not subject to registration in the purchase book;

- the invoice issued by the commissioner in the name of the principals is reflected solely in relation to the amounts used as remuneration for him;

- Accounts drawn up by principals according to information received from commission agents must be registered.

Mediation activities

The main responsibilities of an intermediary include carrying out transactions on his own behalf for money provided by the guarantors, as well as carrying out actions not only for the money of the guarantors, but also on their behalf. The second option involves issuing an invoice either on behalf of the guarantors to the client, or on behalf of the supplier to the guarantors.

Carrying out such operations requires the existence of a guarantee or an agency agreement. There is no need to comply with the rules regarding the preparation of invoices and their storage.

It is possible to carry out operations on behalf of intermediaries if orders are carried out in accordance with commission agreements, agency contracts that provide for the performance of actions by agents on their own behalf.

Simplified diagram

Enterprises operating on the simplified tax system, in some cases, must issue invoices and, as a result, fill out a logbook for their accounting.

According to the decree of July 2019, this is required when products are purchased from a foreign company located abroad, but selling products in the Russian Federation, and also when property assets included in state and municipal funds are leased.

During the 5-day period, a company operating under the simplified system issues an invoice to itself and registers it in the journal.

Correction of documents after delivery

The current legislation does not prescribe the obligation to submit an adjusted accounting journal if it was submitted to the Federal Tax Service, after which shortcomings were discovered in it. However, it is more advisable to correct the errors and send the edited version to the Federal Tax Service.

To make changes to a document, you must first cancel the incorrect invoice. This is done by showing the product price and tax amount with a minus sign and recording the correct version of the invoice with a plus sign.

Let’s say that a product was purchased by an intermediary for a customer, and it was subsequently discovered in his accounting department that the accounting journal for the second quarter contains incorrect details of the invoice received from the seller. The magazine itself has already been sent to the tax office.

In this case, the accountant in the 1st part of the journal cancels the incorrect entry, and the total indicators are indicated with a minus sign. The next line is filled in similarly to the canceled one and the 12th column is corrected, in which the correct account number is indicated. Cost indicators are accompanied by a minus sign.

In the second part of the journal, the incorrect entry is also canceled, but the 4th column in which the account number is corrected is subject to correction. In this case, cost indicators are indicated with a “plus” sign, which serves as confirmation of their reliability.

Attention!

- Due to frequent changes in legislation, information sometimes becomes outdated faster than we can update it on the website.

- All cases are very individual and depend on many factors. Basic information does not guarantee a solution to your specific problems.